Question from Past Microeconomics Qualifying Exam[]

Spring 2004 - Section II, Question one, George Mason University

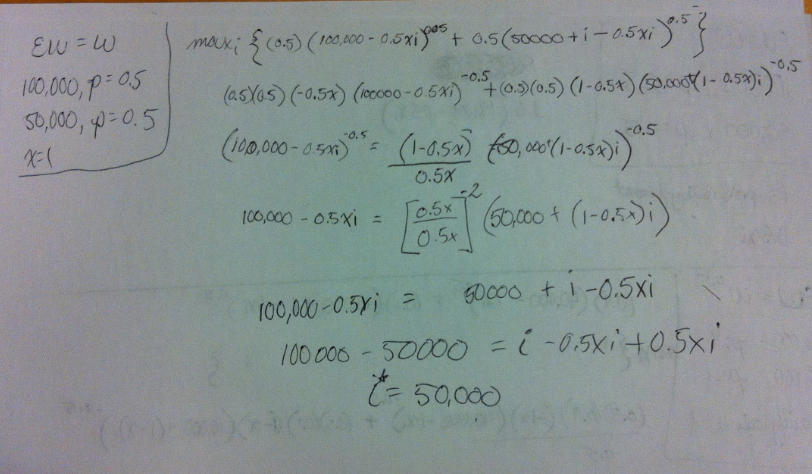

Suppose your EU=w, and insurance is sold at the actuarially fair rate. Your uninsured income is $100,000 with p=.5, and $50,000 with p=.5. Solve for your optimal quantity of insurance, I.

Answer[]

At actuarially fair rates, purchasing $I of insurance will cost 0.5*I. In order to solve for the optimal quantity of insurance, we need to maximize EU in the following setup:

max EU, for EU=0.5(100,000 - 0.5I) + 0.5(50,000 - 0.5I + I)

max EU, for EU=0.5(100,000 - 0.5I) + 0.5(50,000 + 0.5I)

max EU, for 50,000 - 0.25I + 25,000 + 0.25I

max EU, for 75,000

Normally, we would take the first derivative of the above, set equal to zero, and solve for I. However, in this case all the I terms have cancelled out, implying (?) that this individual will not purchase any insurance (self insure). This is intuitively plausible as well, since the person is risk neutral, and has a 50/50 chance of losing half of his income.

{kind=link}

Other Questions[]

- Next MicroS04-II.2

- Previous MicroS04-I.10